On Wednesday, July 17th, the Federal Reserve released the so-called "Beige Book," a regional economic conditions report compiled by the 12 regional Federal Reserve Banks. The report maintained its description of the overall economic activity in the United States at a "slight to modest pace," unchanged from the May report. However, it added that three more regions reported "economic activity being flat or declining," with respondents anticipating a slowdown in economic growth over the next six months.

The Beige Book is published two weeks before the Federal Open Market Committee (FOMC) policy meeting. This edition, compiled by the Federal Reserve Bank of Richmond, summarized information gathered over the six weeks leading up to and including July 8th, encompassing anecdotes and commentary on business conditions in the districts of the 12 regional Federal Reserve Banks.

Regarding "overall economic activity," the Beige Book stated that from late May through June, economic activity in a majority of the Federal Reserve districts experienced slight to modest growth. Seven districts reported an increase in economic activity, while five districts saw flat or declining activity, contrasting with the previous May report, which noted only two districts with unchanged economic activity.

Advertisement

The labor market maintained a "slight pace" of growth in both the May and July Beige Books. Employment rates were flat or "slightly higher" in most regions, with more regions reporting stable or declining rates and only a few regions experiencing "moderate" employment growth. Several regions reported a decrease in manufacturing employment due to a slowdown in new orders.

The scarcity of skilled workers remains a challenge across all regions, particularly in construction, maintenance, retail, healthcare, and tourism sectors. However, several regions have seen improvements in labor supply conditions, with a reduction in labor turnover rates, thus decreasing the need to hire new workers. Some regions anticipate more cautious hiring, not filling all open positions. Businesses continue to turn to automation and outsourcing to save costs and compensate for actual or anticipated labor shortages.

Consequently, in terms of wage trends, wages in most regions increased at a "modest to moderate pace," with several regions noting that enhanced worker availability and reduced competition for labor have slowed wage growth. This description is a slight cooling compared to the May Beige Book, which described wage growth as "mostly maintaining a moderate pace, with a few regions experiencing more modest growth."

On the price front, prices have risen modestly overall, with some regions reporting only slight increases, consistent with the May report. Notably:

"Despite widespread reports of little change in consumer spending, almost every region mentioned retailers discounting goods or price-sensitive consumers purchasing only necessities, opting for lower quality, buying fewer items, or shopping around for the best deals.

Most regions noted that input costs began to stabilize; however, the Atlanta Fed district specifically pointed out significant increases in products such as copper and electrical goods during this period.

As demand wanes, businesses' ability to raise prices without alienating customers diminishes. While food and commodity costs have remained largely unchanged, increases in freight and some building materials' prices have been observed."Specifically, in terms of consumer spending, the statistics from most Federal Reserve districts show little change in household expenditures this quarter, while the situation of automobile sales varies across regions. Some areas have noted a decline in car sales due to dealerships being hit by cyberattacks and persistently high loan interest rates. Travel and tourism have seen steady growth, in line with seasonal expectations.

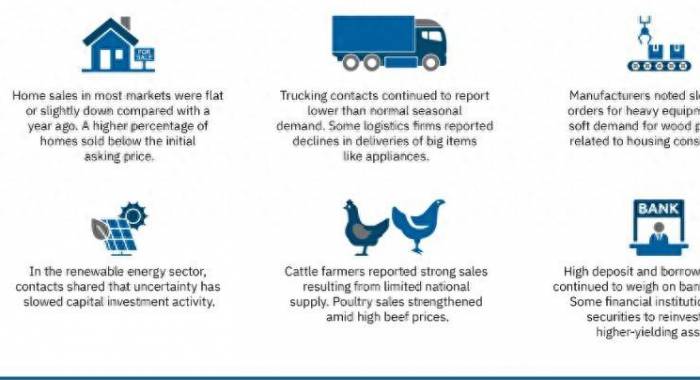

In the banking and financial sector, there is soft demand for consumer and commercial loans in most regions, but overall loan demand remains moderate, with a slight increase in specific loan types, such as home equity loans and used car loans. Deposits continue to decline slightly.

The residential and commercial real estate markets have seen only minor changes in recent weeks. The residential real estate market is showing a typical seasonal slowdown, with inventory gradually increasing. Commercial real estate activity varies, with retail leasing picking up, but office leasing remains weak:

"Due to housing prices being close to peak levels and interest rates remaining high, the volume of residential sales in most markets is flat or slightly down compared to the same period last year. A higher proportion of homes are being sold at prices below the initial asking price, indicating a market shift towards buyers.

Commercial real estate activity is mixed. Slowdowns in office and apartment markets have led to increased vacancy rates, flat or declining rent growth, and increased foreclosure rates in these sectors."

Manufacturing activity across regions is mixed, with descriptions ranging from a "brisk downturn" to "moderate growth." Some areas have noted weak demand for manufacturing products. Overall, manufacturing activity has declined slightly since the May Beige Book, with some regions experiencing a slowdown in new heavy equipment orders and weakening demand for wood products related to homebuilding.

Agricultural conditions have improved slightly, with cattle farmers reporting strong sales and higher beef prices boosting optimism among poultry farmers. However, demand for some row crops like cotton remains weak, and agriculture is also affected by sporadic droughts across the country.

In addition, restocking in the retail sector has stimulated a slight increase in transportation activity, with tight ocean shipping capacity leading to soaring spot freight rates. However, trucking contacts continue to report seasonal demand below normal levels, with some logistics companies stating that direct-to-consumer (DTC) deliveries of bulk items such as wholesale, retail, and home appliances have declined. Warehousing contacts report a slowdown in demand for distribution and storage space.

Notably, the Beige Book also discusses the expansion of AI technology investment:

"Utility contacts report that electricity demand in the commercial and industrial sectors is increasing, primarily attributed to new and expanded data center projects, which focus on the increasing use of artificial intelligence technology."Contacts in the renewable energy sector have indicated that the uncertainty surrounding the U.S. presidential election has slowed down capital investment activities.

Overall, respondents' short-term outlook is not optimistic:

"Due to the upcoming U.S. presidential election, domestic policies, geopolitical conflicts, and uncertainties surrounding inflation, expectations for the economy over the next six months are for slower growth."

Analysts have stated that the latest Beige Book indicates that the overall economic activity in the U.S. remains positive but shows signs of slowing down. Consumer spending is stable but not increasing, and consumers are more sensitive to prices. The economy is still growing, but at a slow pace, and there are increasing signs of stagnation or decline:

"This may be a sign of a soft landing, but remember, every hard landing starts with a soft landing."

Following the release of the Beige Book, the U.S. Dollar Index DXY continued to decline during the day, holding near the four-month low since late March. The major U.S. stock indices also maintained their earlier trends, with only the Dow Jones, which is heavy with blue-chip stocks, rising, while the Nasdaq and S&P technology sectors are on track for their worst performance since 2022. The two-year U.S. Treasury yield also fell in the short term, trading at a five-month low, and the 10-year benchmark bond yield hovered at a four-month low.

Leave A Comment